What it is

Renewal, switch, or refinance guidance

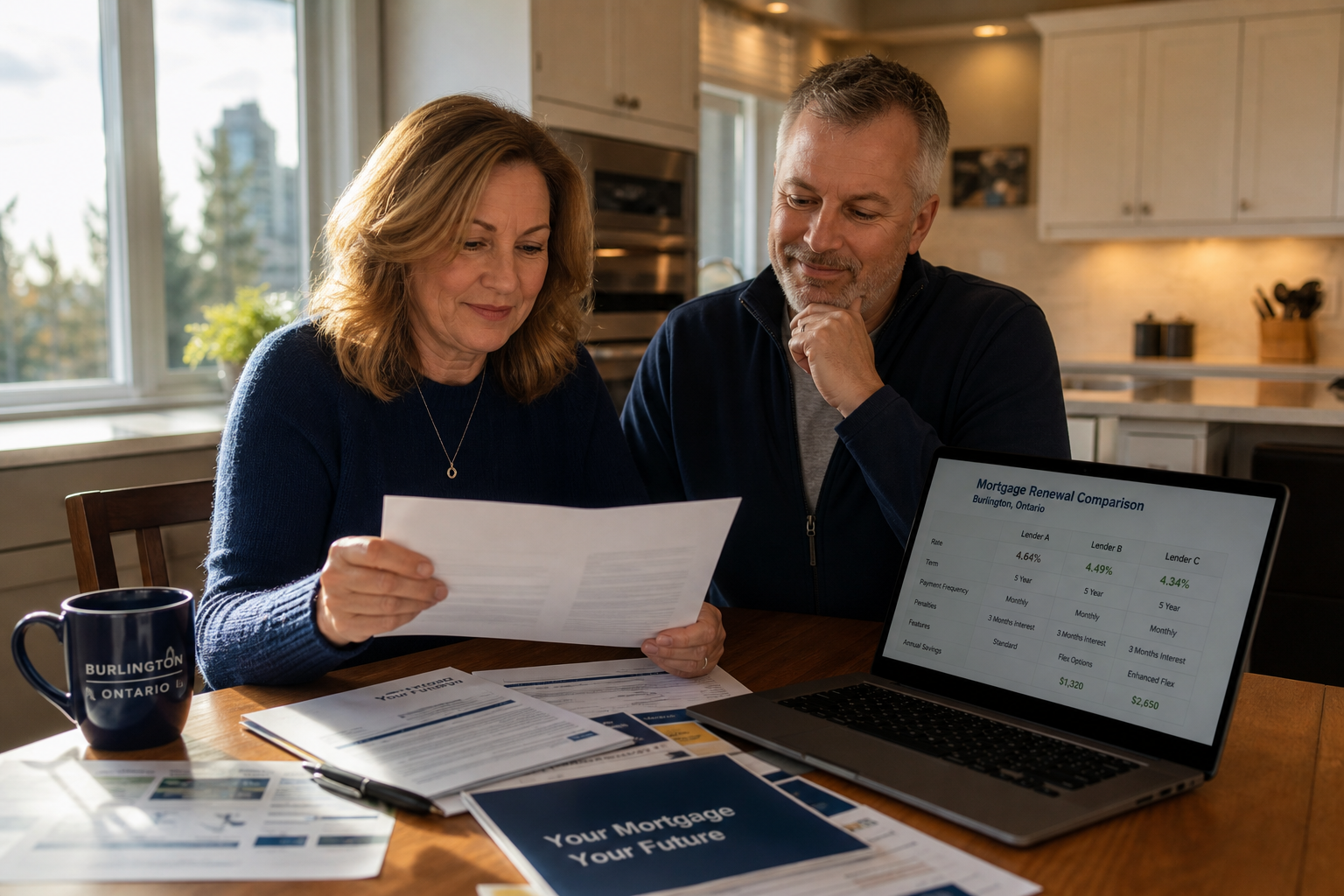

Mortgage Renewal Review in Burlington

Your mortgage term is ending. What now?

Your mortgage term is ending. What now? A mortgage renewal review compares your current lender’s offer against realistic alternatives. The best option may be to renew, switch lenders, or refinance depending on your rate, penalty, mortgage balance, equity, income, credit, and whether you need additional funds.

First lender review

We show you the real cost of each path: renew, switch, or refinance with your actual numbers.

Key mortgage facts

A renewal offer should be compared before it is signed

Most lenders review income, credit, property details, down payment or equity, documents, and the lender lane that matches the file.

File signals

Homeowners approaching their renewal date who want to compare options...

Homeowners approaching their renewal date who want to compare options before signingOntario review

Ontario switch files require clean timing around renewal windows, discharge...

Ontario switch files require clean timing around renewal windows, discharge rules, insurance proof, and property-tax detailsBroker role

Compare the realistic lender lanes

The renewal offer is convenient, but convenience is not the same as fit. A quick comparison can show whether staying, switching, or refinancing is actually better.File fit

Borrower and property signals lenders review

Lender choice usually turns on documented income, credit history, equity or down payment, property type, timing, and whether the file needs prime, alternative, or private review.

Stronger file signals

Usually stronger when

- Homeowners approaching their renewal date who want to compare options before signing

- Borrowers who suspect their lender renewal offer is not competitive with the market

- Households whose payment comfort, moving plans, or financial goals have changed since the last term

Different route

A different lender path may be cleaner when

- Borrowers who need to add funds, change amortization, or restructure debt: this is a refinance conversation, not a renewal review

- Files under urgent hardship, bank decline, or credit pressure: start on the Bank Said No or Bad Credit pages first

- First-time home buyers who need a purchase mortgage: start on the Purchase or Pre-Approval page

Straight answers

Renewal and switch rules to compare

A renewal letter is an offer. The practical answer is that homeowners should compare renewal, switch, and refinance paths before signing.

What should homeowners compare at renewal?

At renewal, homeowners should compare the offered rate, term, payment, penalty formula, prepayment privileges, portability, and whether a switch or refinance is better. Canada.ca notes that federally regulated lenders must send a renewal statement at least 21 days before the term ends, but borrowers do not have to wait for that statement to shop. Starting earlier gives time to compare lenders and avoid a rushed signature.

Source: Canada.ca mortgage renewal guidanceDoes the stress test apply when switching lenders at renewal?

OSFI no longer expects federally regulated lenders to apply the minimum qualifying rate to uninsured straight switches at renewal, as long as the loan amount and amortization do not increase. That does not mean every switch is automatic. The new lender still reviews the file under sound underwriting principles, and adding new money, extending amortization, or adding secured credit can turn the request into a refinance.

Source: OSFI uninsured straight-switch guidanceOntario renewal context

A renewal letter should be compared, not just signed

Renewal is the point where Ontario homeowners can compare staying, switching, or refinancing before the next term locks in.

Renewal notice timing

At least 21 daysFederally regulated lenders must send a renewal statement at least 21 days before the end of the term.

Source: Canada.caUninsured straight switch

MQR exemptionOSFI no longer expects the prescribed minimum qualifying rate on uninsured straight switches with no increase to loan amount or remaining amortization.

Source: OSFIStructure comparison

Renew / switch / refinanceA renewal keeps the mortgage in place, a switch moves lenders at maturity, and a refinance changes the loan structure or balance.

Source: Canada.caFile strength

What can strengthen a renewal review?

Renewal is a good time to check the entire mortgage strategy, not just the rate on the letter.

Current renewal offer and mortgage statement

Updated income and debt picture if switching or refinancing is possible

Clear goal for the next term: payment stability, flexibility, or equity access

Penalty and discharge information from the current lender

Property value estimate and remaining amortization

Timeline of at least 90-120 days before maturity when possible

Lender paths

Renewal paths compared

A renewal review should compare staying, switching, and refinancing with the costs and requalification requirements visible.

| Lender path | Best fit | What lenders review | Trade-off |

|---|---|---|---|

| Renew with current lender | Simple file and acceptable offer | Usually lighter if no major changes are requested | Easy, but may leave better options untested. |

| Switch lenders | Better rate or structure without taking new funds | Income, property, and credit review by the new lender | May require requalification, legal, appraisal, or discharge steps. |

| Refinance | Debt consolidation, renovations, or equity access | Full application and updated property value | More moving parts, but can solve bigger financial goals. |

| Alternative path | Files that no longer fit prime lending | Full story, equity, and exit plan | Higher cost; useful when the current option is no longer workable. |

Path

Renew with current lender

- Best fit

- Simple file and acceptable offer

- Review focus

- Usually lighter if no major changes are requested

- Trade-off

- Easy, but may leave better options untested.

Path

Switch lenders

- Best fit

- Better rate or structure without taking new funds

- Review focus

- Income, property, and credit review by the new lender

- Trade-off

- May require requalification, legal, appraisal, or discharge steps.

Path

Refinance

- Best fit

- Debt consolidation, renovations, or equity access

- Review focus

- Full application and updated property value

- Trade-off

- More moving parts, but can solve bigger financial goals.

Path

Alternative path

- Best fit

- Files that no longer fit prime lending

- Review focus

- Full story, equity, and exit plan

- Trade-off

- Higher cost; useful when the current option is no longer workable.

Compare the lender path

Most Ontario borrowers have more than one possible lender path. The useful question is which path fits the file, timeline, and risk tolerance.

Before you sign

Compare the renewal offer before it becomes the default

A renewal letter can arrive when life is busy. The best time to compare options is before the maturity date forces a rushed decision.

Renew

Often simplest when the offer is competitive and no new money is needed.

Switch

Can improve rate or terms, but the new lender must approve the file.

Refinance

Useful when debts, renovations, or equity access are part of the decision.

Important review notes

Self-employed and renewing?

Switching lenders may require a fresh income review, especially if your tax returns, write-offs, or corporation make the file harder to read. Start with a renewal review before assuming your current lender is your only option.

Things to know

Common mistakes to avoid before choosing this path

These are the points that usually create delays, poor lender fit, or a mortgage structure that looks fine at signing but weakens the longer-term plan.

Do not judge the file by rate alone

The lowest renewal rate is not always the best choice if portability, prepayment rights, or penalty terms are weak

Do not wait to organize documents

Most lenders will ask for proof such as current mortgage statement or renewal letter from your lender. The cleaner the document package, the easier it is to compare options without rework.

Do not ignore Ontario-specific costs or rules

Burlington homeowners planning to move, refinance, or access equity within the next few years should choose the term around that timeline, not just the lowest rate

Plan ahead

A renewal offer should be compared before it is signed

Signing a renewal letter takes five minutes. Comparing your options takes one conversation. Most homeowners save money by understanding the difference between renewing, switching, and refinancing before the deadline arrives.

5

Steps

We review your current mortgage statement, renewal...

5

Documents

Current mortgage statement or renewal letter from...

6

FAQs

Should I sign my lender renewal...

Use the Mortgage Calculator

Estimates are educational. We can help turn them into a real mortgage strategy.

Service snapshot

Clear details before you decide how to proceed.

We show you the real cost of each path: renew, switch, or refinance with your actual numbers.

That means comparing the rate, penalties, legal fees, incentives, and whether a change in balance or structure actually solves a problem you have today.

01

Why auto-renewing is usually the most expensive option

Not before comparing it. Renewal is the easiest time to review rate, term, payment,...

02

How to tell if switching lenders is worth the paperwork

Start a few months before maturity so there is time to compare, gather documents,...

03

When refinancing makes more sense than a simple renewal

Renewing keeps the mortgage with your lender, switching moves the same mortgage balance, and...

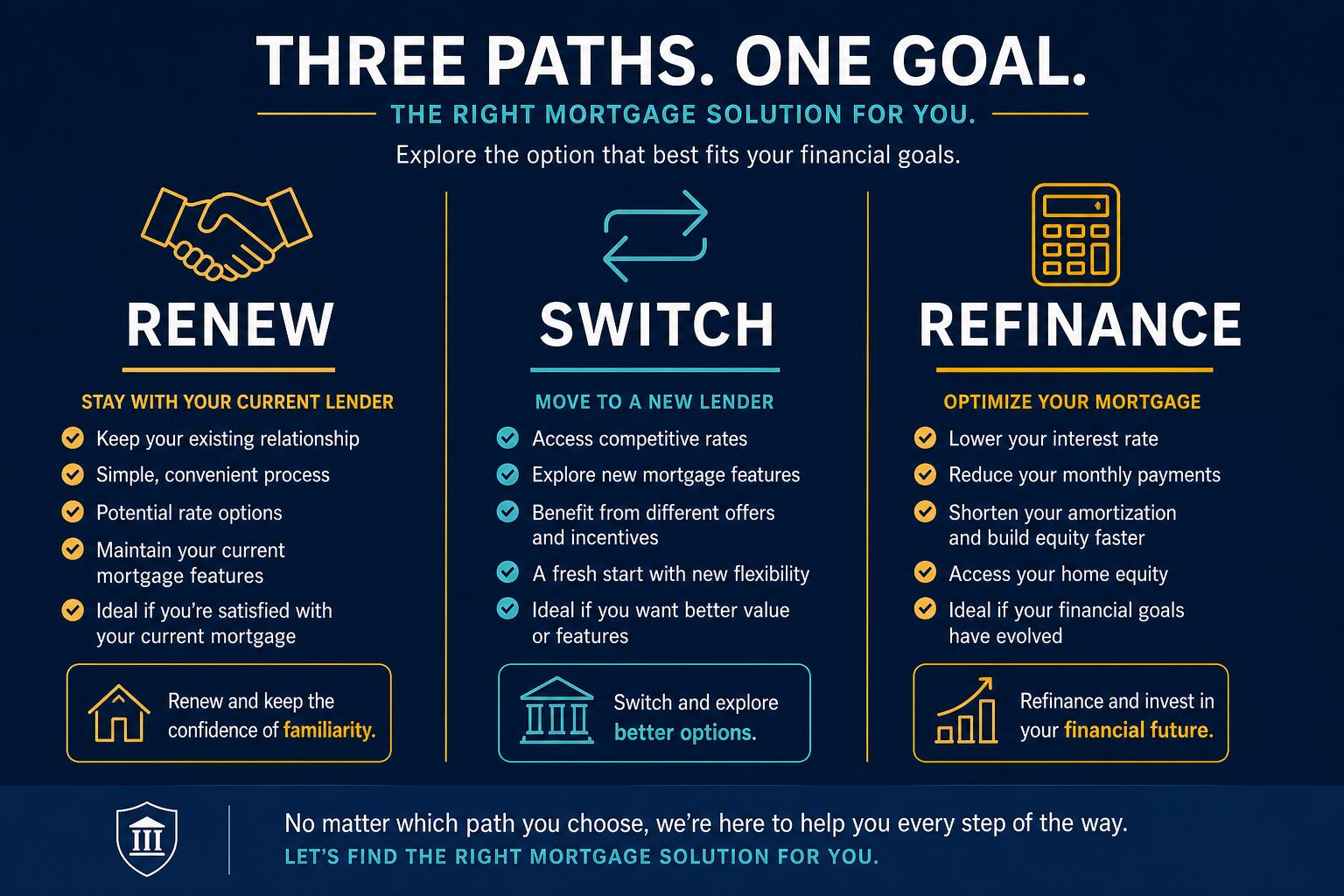

Your three options

Renew. Switch. Refinance.

What is the difference?

Each path changes something different about your mortgage. Here is the simplest breakdown you will find.

Renew

Stay with your current lender. Change only the term length and rate. No new documentation or qualification needed. Simplest path, but often the most expensive rate.

Fastest. Least paperwork.

May not be the most competitive offer.

Switch

Move your mortgage to a new lender for a better rate. Same balance, same home, better terms. Some paperwork required, but lenders often cover the switch costs.

Often more competitive when the file fits.

Allow time before maturity.

Refinance

Change your mortgage balance, rate, and structure. Access equity, consolidate debt, or lower payments by extending amortization. More paperwork but more flexibility.

Changes balance. Accesses equity.

Full qualification needed.

Renew, switch, and refinance use different approval rules. We compare the three paths with your actual numbers. Tell us about your situation and we will show you which path is strongest after costs and lender requirements.

Compare what each path means

How renew, switch, and refinance stack up.

The right choice depends on your rate, what you want to change, and your timeline.

| Factor | Renew | Switch | Refinance |

|---|---|---|---|

| Mortgage balance | Stays the same | Stays the same | Can increase or restructure |

| Interest rate | Lender offer (usually higher) | Competitive market rate | Competitive market rate |

| Credit check needed | Usually not | Yes (one inquiry) | Yes (one inquiry) |

| Income documents needed | No | Yes (re-qualification) | Yes (full re-qualification) |

| Typical cost | Usually lowest friction | May involve discharge, legal, appraisal, or admin costs | More setup costs and a fuller underwriting review |

| Timeline | Days (sign the letter) | Needs time for the new lender to review and instruct | Needs enough time for full approval, valuation, and legal work |

| Best for people who | Are happy with their rate and want the fastest possible path | Want a lower rate and do not need to change their balance | Need to access equity, consolidate debt, or change their mortgage structure |

Real talk: A switch can save money when the new lender offer is meaningfully better after all costs. A refinance makes sense when you need to change the mortgage balance, amortization, or structure, not just when you want a different rate.

How to decide

Three questions to ask yourself.

Answer these honestly, and the right path becomes obvious.

1

Is your renewal offer competitive?

Compare your offered rate, term, penalties, and flexibility against current lender options. If the offer is meaningfully weaker after costs, switching may be worth reviewing.

If yes: renew. If not: consider switching.

2

Do you need to change your mortgage?

Want to borrow more for renovations or debt consolidation? Need to extend amortization? That is a refinance, not a renewal.

If yes: refinance. If no: switch or renew.

3

Do you plan to move or sell soon?

If you might sell soon, portability, penalty exposure, and term length matter. Avoid choosing a longer fixed term only because it looks simple today.

If yes: short term or portable. If no: longer term is fine.

Cost clarity

What switching or refinancing actually costs.

Costs vary by lender, mortgage type, property, and whether you are switching at maturity or changing the mortgage structure. We compare the real net benefit before you move.

Legal / admin fees

File-specific

Legal, registration, and administration costs depend on the lender path and whether a switch program covers eligible setup work.

Discharge fee

Lender-specific

Your current lender may charge discharge or administration costs. The exact amount should be confirmed from the payout statement.

Appraisal (if needed)

If required

Some lenders need a current property value. Others may use automated valuation or waive the appraisal on straightforward files.

The useful question: net benefit after costs

Some lenders may cover eligible switch costs or offer incentives, but the real comparison is the rate, term, penalty risk, setup costs, and whether the new lender can approve the file cleanly.

Renewal approval steps

From renewal letter to confident decision in 5 steps.

The review checks the renewal offer, switch options, refinance costs, lender requirements, and timing before the maturity date.

1

We review your current mortgage statement, renewal letter, and your goals

2

We pull current rates and compare them to your renewal offer

3

We explain the three options with your real numbers: renew, switch, or refinance

4

If switching, we calculate the net savings after fees and coordinate timing with your closing date

5

We handle the paperwork, conditions, and final sign-off so you feel confident before the term ends

Common questions

Renewal, switch, and refinance questions in Ontario

Plain answers on renewal offers, switching lenders, stress-test rules, penalties, and when a refinance belongs in the conversation.

Should I sign my lender renewal offer?Not before comparing it. Renewal is the easiest time to review rate, term, payment, penalties, and lender fit.+

The renewal letter is an offer, not your only option. Before signing, compare competing lenders, term lengths, fixed versus variable, payment flexibility, prepayment privileges, and penalty structure. Even if you stay with the same lender, comparison gives you better context for negotiation.

How early should I start shopping for renewal?Start a few months before maturity so there is time to compare, gather documents, and switch if another lender fits better.+

Starting early keeps you from being rushed by the renewal deadline. It gives time to compare rates and terms, confirm whether a switch makes sense, review any collateral-charge issues, and prepare documents if the new lender needs a full application.

What is the difference between renewing, switching, and refinancing?Renewing keeps the mortgage with your lender, switching moves the same mortgage balance, and refinancing changes the loan amount or structure.+

A renewal usually means accepting a new term with your current lender. A switch or transfer moves the mortgage to another lender, generally for the same balance and amortization. A refinance changes the mortgage amount, amortization, or purpose, often to access equity or consolidate debt.

Do I need to pass the stress test when switching lenders at renewal?For many uninsured straight switches between federally regulated lenders, OSFI does not expect the minimum qualifying rate to apply if the loan amount and amortization do not increase.+

OSFI says the minimum qualifying rate is generally not expected for uninsured straight switches at renewal when the borrower moves from one federally regulated lender to another with no increase to the loan amount or amortization. Lenders still underwrite the file, and changes such as new money, longer amortization, or a HELOC can change the review.

When should I refinance instead of simply renewing?Consider refinancing if you need equity, debt consolidation, a new amortization, or a materially different mortgage structure.+

A simple renewal is often enough when the balance, payment, and structure still fit. A refinance enters the conversation when you need cash out, want to consolidate higher-interest debt, need to restructure payments, or want to solve a problem the current mortgage cannot solve. The trade-off is that refinancing may require full qualification and extra costs.

Can I switch lenders if my mortgage has a collateral charge?Often yes, but it may involve more legal work or fees than a standard charge mortgage.+

Collateral charges can make switching less automatic because the existing charge may need to be discharged and replaced. The cost depends on the lender, registration, and whether other loans or lines of credit are secured by the same charge. We check this before recommending a switch.

Related guidance

Not on this page? The answer may be here.

If renewing, switching, or refinancing is not quite what you need, one of these pages may be a better starting point.

Next step

Refinance Guidance

Use this page if the real goal is changing your mortgage balance, amortization, or structure instead of simply renewing on the same terms.

Go to pageNext step

Self-Employed Renewal Review

Start here if switching lenders may depend on business income, write-offs, or incorporated income documentation.

Go to pageNext step

HELOC and Home Equity Options

Best next stop when renewal decisions overlap with wanting to access equity through a HELOC, second mortgage, or cash-out refinance.

Go to pageNext step

Bank Said No? Mortgage Options

Go here if your renewal was denied or your current lender offered unworkable terms and you need alternative lending guidance.

Go to pageNext step

Purchase Mortgage Guidance

Use this page when the next step is buying a new home and the renewal decision is really about portability and timing your move.

Go to pageCompare the renewal path

Not sure whether to renew, switch, or refinance?

We can review your renewal letter, compare it to the market, and tell you which path makes the most sense for your situation. One conversation, clear answers, no pressure.